New build container vessels exploding industry insight

In ocean shipping, present success often breeds future failure. Across the decades, freight-rate spikes have spurred newbuilding sprees, wiping out freight rates. Which brings us to today: Container freight rates are spiking and container-ship newbuild orders are surging at yards in China, South Korea and Japan. Is the ending of this story inevitable?

Not necessarily. There have been a very large number of orders in Q4 2020 and Q1 2021. Yet container shipping’s orderbook was historically low before this new wave of contracts hit.

What happens next will be important to watch. Not only for investors in container shipping, but for tanker and dry bulk investors, as well.

Despite new build orders, carriers worried about future CO2 rules

It has long been argued that shipowners are abstaining from orders because they fear future decarbonization rules won’t grandfather in today’s carbon-emitting newbuild designs. What’s happening now in container shipping implies that owners can overcome this fear if returns look high enough.

“Turns out, when things are good, people will still order even if they are concerned what type of fuel to use,” wrote Stifel analyst Ben Nolan.

Alphaliner analysis that orderbook-to-fleet ratio still running short

According to the latest figures from Alphaliner, the orderbook as of Friday was 401 container ships totalling 3.63 million twenty-foot equivalent units (TEUs).

The orderbook is 15.3% of the on-the-water fleet’s capacity measured in TEUs, up from a multi-decade low of just 9.4% in mid-2020.

However, today’s ratio pales in comparison to an orderbook-to-fleet ratio of over 60% in 2008. “An orderbook of 15% of the fleet is normal,” assured Stefan Verberckmoes, shipping analyst and Europe editor at Alphaliner, in an interview with American Shipper. This is an orderbook level that makes sense to renew the fleet and handle annual cargo growth.

Shipping Lines observe through full the global ships orderbook

Rolf Habben Jansen, CEO of Hapag-Lloyd, made the same point during his company’s call with analysts on Thursday. “We are nowhere near the situation we saw in 2007-2008, when we saw the orderbook that was more than half the global fleet.

Today, we are concerned when we look at 12% [his estimate was below Alphaliner’s current number].

I would say it’s probably going to hover around a number that’s slightly better than that. But that would still allow us to be in reasonably healthy territory.”

The problem for container shipping would arise if the orders keep coming. Verberckmoes warned, “If the orders continue at the same pace in Q2 and if we see speculative orders coming in, and it goes from 15% to 20%-30%, then it becomes worrisome. Because we don’t have any visibility on the cargo demand a few years from now.”

Megamax vessel of plus 18.000 TEU orders dominate Q4 2020

As previously reported by American Shipper, Q4 2020 container-ship orders were dominated by so-called “megamaxes,” vessels with capacity of over 18,000 TEUs and 23-24 container rows on deck. Most of the 25 orders were for carriers that didn’t have enough megamax capacity. These were mostly orders that had been previously expected.

For 2020 overall, almost all of the orders were for megamaxes or for smaller ships (2,500 TEU or below) used primarily for intra-Asia trades. There were only a few “neo-Panamaxes” — ships of 12,000-16,000 TEU with 20 container rows on deck that can traverse the new Panama Canal locks. There were virtually no orders in the midsize 5,000- to 9,000-TEU categories. Newbuilds were either very big or very small.

In contrast, Q1 2021 has seen four more megamax orders and ongoing orders for smaller ships, but a surge in orders for neo-Panamaxes — 60 so far with at least nine more possible by the end of March. “There is a very clear preference for neo-Panamax ships,” reported Verberckmoes.

Maxi Panamax type vessels offer carriers highest flexibility

“Some are 13,000 TEU but most are 15,000-15,900 TEU. We can now see that these ships are going to be the workhorses of the sector, comparable to the maxi-Panamax [up to 5,100 TEU] ships that went through the old Panama locks.

“Carriers are asking: What is the ideal ship of the future, versatile enough to be used in a lot of trades? The answer, mostly, is the biggest ship possible to transit the Panama Canal.”

The 14,414-TEU neo-Panamax CMA CGM Theodore Roosevelt, an example of ‘the new workhorse’.

In the larger categories, owners are ordering either megamaxes or neo-Panamaxes, “but nothing in between,” he continued. “Nobody is ordering 18,000-TEU ships. And I strongly feel that nothing will be ordered [in this size], simply because it doesn’t make sense.

“You will have ships in Far East-Europe and you’ll want the biggest ships — 24,000 TEUs. Or you’ll want the flexibility and you’ll go for 15,000-15,900 TEUs, which you can deploy on virtually all trades.

“You can put them in the trans-Pacific via Panama, on Asia-Latin American, on Asia-West Africa. There is even a 15,000-TEU ship now going from India to the U.S. East Coast.”

Choice between LNG fuels or scrubber fitted vessels remains undecided

The common wisdom is that new orders in any shipping segment favor designs allowing for liquefied natural gas (LNG) as fuel. LNG is viewed as a transitional choice before the switch to the new generation of fuels necessary to meet the International Maritime Organization’s 2050 decarbonization goal.

But this theory is not playing out in container shipping, the one segment where current fundamentals justify large-scale newbuild orders.

“We have only seen three carriers going for LNG: CMA CGM, Hapag-Lloyd and ZIM,” said Verberckmoes. ZIM (NYSE: ZIM) opted for LNG fuel for newbuilds chartered from Seaspan, a division of Atlas Corp. (NYSE: ATCO).

CMA CGM LNG-powered newbuild (Photo: CMA CGM). “All the others are scrubber-fitted,” he said.

Scrubber-fitted newbuilds allow the consumption of cheaper 3.5% sulfur fuel known as high sulfur fuel oil (HSFO), whereas non-scrubber ships must consume more expensive 0.5% sulfur fuel known as very low sulfur fuel oil (VLSFO). It is much more economical to install scrubbers in newbuilds than to retrofit them into existing ships.

Alternative fuels are not an option as they are currently not orderable

Asked why so many container-ship owners would order ships despite the looming specter of decarbonization rules, he replied: because “there is no alternative.”

“Methanol ships are in development. There are trials with ammonia. There are studies of ships with hydrogen. None of these ships are orderable yet. If you are a carrier like MSC that expects 3% [demand] growth per year, you need to add to your fleet.

And the only options right now are LNG or scrubbers and using dirty fuel oil. Some may look at LNG and say it’s still a fossil fuel, so they just decide to go with scrubbers.”

“Maersk said, ‘OK, we are not going to expand the fleet [until there is a carbon-neutral newbuild option].’ But they are the only ones in the industry taking this approach.”

Shipping lines favour leasing and not owing vessels

Liner companies own a portion of their fleets and charter in the rest from non-operating owners (NOOs).

U.S.-listed NOOs include Atlas Corp., Danaos (NYSE: DAC), Costamare (NYSE: CMRE), Global Ship Lease (NYSE: GSL), Navios Containers (NASDAQ: NMCI), Navios Partners (NYSE: NMM), Capital Product Partners (NASDAQ: CPLP) and Euroseas (NASDAQ: ESEA).

According to Verberckmoes, “The main orderers are the NOOs, companies like Seaspan, Zodiac, Eastern Pacific and Capital Maritime. Carriers such as Evergreen, OOCL and Hapag-Lloyd accounted only for about one-fifth of all orders in Q4 and Q1. This is the same tendency we’ve seen for a number of years.”

Seaspan leading the pack with order book for 31 newbuildings

Atlas Corp.’s Seaspan has been particularly aggressive. It has ordered 31 newbuildings since December with an aggregate capacity of 451,000 TEUs, all with charters attached for durations ranging from six to 18 years.

“For the carriers, there’s a very good case for time-chartering these neo-Panamaxes from the NOOs,” explained Verberckmoes. “If you charter them, you don’t have to pay for them all at once. You can replace your 8,000-TEU ships that are 20 years old and are obliged to burn more-expensive VLSFO with a 16,000-TEU ship with a scrubber, so you can burn heavy fuel oil [HSFO].

“And if you replace two 8,000-TEU ships with one 16,000-TEU ship, economies of scale not only give a lower per-slot cost. They also reduce CO2 emissions per TEU. That is why MSC says its biggest megamaxes are its most environmentally friendly ships.”

Shipping industry concerned about possible speculative ships orders

Newbuilding orders by liner companies — or by NOOs with long-term charters to liners — do not raise red flags. What will raise red flags is speculative orders by NOOs with no charters attached.

The Alphaliner analyst emphasized, “The big question is whether there will be speculative orders, whether Greek or other companies will just say, ‘OK, we feel there will be a market for these ships. We will order them even though we don’t have a charter yet.’

“That is the big question that still remains unanswered. We have some orders where we cannot yet see the charterer, so they could be speculative. But we don’t have any evidence yet of speculative orders.”

He cautioned, “We could see the repeat of the old mistake of carriers [and NOOs] ordering too many ships. We should not forget that the shortage of ships is also partly due to congestion, with an average waiting time at anchor in Los Angeles/Long Beach of over seven days. If only the problem in Los Angeles/Long Beach is solved, it will already bring around 30 big ships back on the market. That’s a lot of capacity coming back.”

Transpacific ports may expect to handle more larger vessels of 15.000 TEU in near future

Today’s orderbook trends offer an important signal to the world’s ports. If you’re handling mostly midsized 5,000- to 9,000-vessels, expect to service ships twice that size in the years ahead.

“Nothing is being scrapped,” said Verberckmoes. “All the ships are being chartered. All the ships are still around. But if the market falls down or when a new wave of neo-Panamax ships hits the waters, there are candidates for scrapping,” he noted.

“It’s clear that most ports are ready to handle 15,000-TEU ships. And there are a lot of 7,000-, 8,000-, 9,000-TEU ships still active in the trans-Pacific. They are getting older and they can easily be replaced.”

Alphaliner sents warning to shippers : do not expect vessels capacities will be restored shortly

There are not enough ships in existence to handle today’s containerized cargo demand. Thus, every new vessel order is a plus for importers and exporters. “Cargo owners would hope that there are even more orders and there will be overcapacity and prices will go back down again,” said Verberckmoes.

But recent orders are mostly for delivery in 2023. Shippers still face years of the vessel-supply status quo before a big wave of fresh capacity hits.

Fearnleys Securities estimates that global volumes will increase 6% this year, while capacity will only increase 3%. Alphaliner net expects fleet growth of 3.7%. Clearly, this supply-demand outlook offers no relief from historically elevated spot rates.

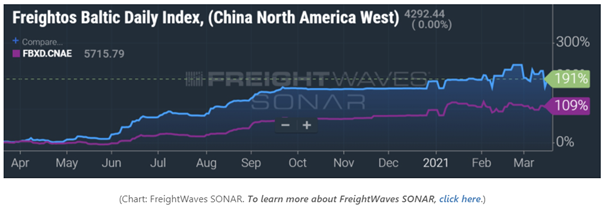

As of Thursday, Asia-West Coast spot rates (SONAR: FBXD.CNAW) were at $4,292 per forty-foot equivalent unit (FEU), up 191% year-on-year, according to the Freightos Baltic Daily Index. Asia-East Coast rates (SONAR: FBXD.CNAW) were $5,716 per FEU, up 109% year-on-year.

Vessels orderbook not sufficient to cover cargo demand through 2023

The longer-term question for cargo shippers is whether larger fleets will compel liners to go for market share and compete more on price, i.e., whether liners’ current capacity-management discipline will ultimately break down.

What this means to stock investors? The NOOs face the highest long-term risk from overcapacity. When markets collapse, as most recently occurred in 2016, charters get renegotiated or canceled.

“In the past, when volumes went down, the first thing carriers did was return chartered ships. So, the problem was not with the carriers, it was with the NOOs,” said Verberckmoes.

Given newbuild lead times, this potential risk is still years away. Furthermore, the orderbook is actually still too low, according to Fearnleys. It estimates that the orderbook-to-fleet ratio needs to grow to 17% just to cover cargo demand through 2023.

Questions rise in respect of dry bulk and tanker investments

For dry bulk and tanker investors, the container-ship ordering spree raises the question: What if the thesis that owners won’t order because of fear of decarbonization rules is actually owners “talking their book?”

What if bulker and tanker newbuilds will be ordered regardless of regulatory concerns, whether to enhance vessel efficiency to comply with looming efficiency rules, to add LNG fuel capability or to install scrubbers and take advantage of the re-widening VLSFO-HFO spread?

As Deutsche Bank transportation analyst Amit Mehrotra told American Shipper in a recent interview, for commodity ship owners to go on an ordering binge, “rates would need to be much stronger for much longer than people think today,” “second-hand asset values would need to be a lot higher,” and consequently, “equities would have to be significantly higher.”

In other words, dry bulk and tanker markets would have to be as red-hot as container markets are now — which would be a highly lucrative “problem” for dry bulk and tanker investors to have.